Imagine you walk into a warehouse packed with boxes. Some are new, others dusty from last year. You need to record the value of your stock. Which boxes do you count first?

That’s where the LIFO vs. FIFO debate begins. These two inventory methods decide how costs move through your books. The choice can affect profits, taxes, and even how investors see your business, which is why accounting experts help small businesses choose the right method to stay compliant and profitable.

Inventory management is not only about counting items. It’s about choosing a method that fits your goals and tells a clear story about your operations.

FIFO and LIFO: The Basics in Plain English

Every business that holds stock must assign a value to its inventory. This valuation helps determine the cost of goods sold (COGS) and the worth of remaining stock at the end of an accounting period.

Accurate valuation is important because it affects not just profit margins, but also taxes and business performance analysis. That’s why integrating POS with accounting systems can streamline tracking, ensure accuracy, and simplify financial reporting.

Inventory valuation methods are the rules a company follows to calculate how inventory costs flow from stock to expenses. Choosing the right method ensures that financial statements truly reflect a business’s real costs and profits.

FIFO (First-in, First-out) — The Logical Choice

FIFO means the first items bought are the first items sold. Older inventory goes out first.

Quick facts:

- Matches how most businesses operate in real life.

- Works well when prices are rising.

- Often shows higher profit since older, cheaper stock is sold first.

LIFO (Last-in, First-out) — The Cost-focused Strategy

LIFO means the latest items bought are sold first. The newest stock gets used before the old.

Quick facts:

- Used mainly in the U.S. under GAAP rules.

- Reduces taxable income in times of inflation.

- Can show lower profits since recent, higher costs are used first.

A Simple Analogy

Think about your fridge:

- FIFO: You drink the milk you bought last week before the new one.

- LIFO: You open the new bottle first because it’s easier to grab.

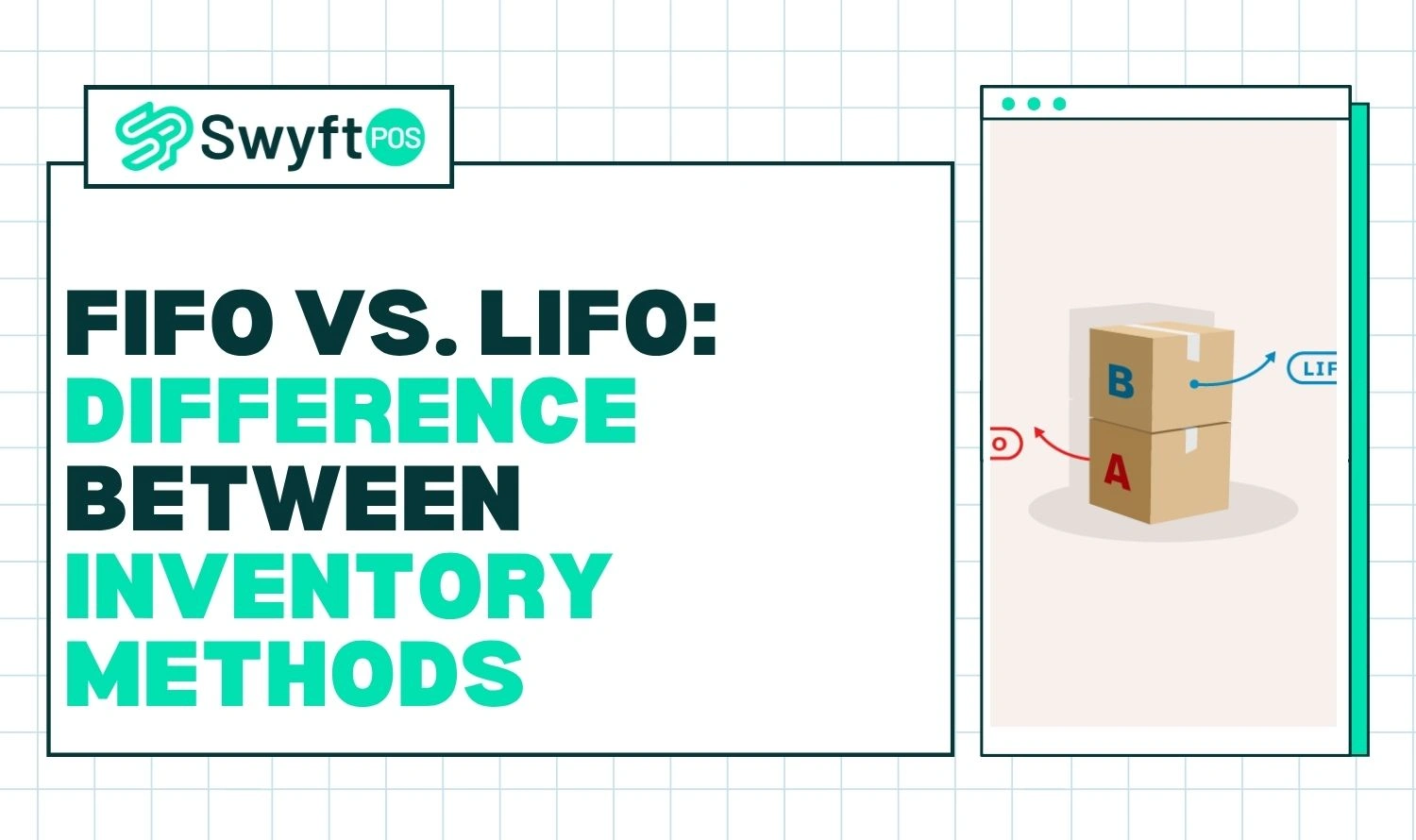

Head-to-Head Showdown — FIFO v. LIFO

Now that you know the basics, let’s see how these two methods stack up side by side. This quick table makes it easier to spot where they differ and how each one affects your numbers.

| Feature | FIFO | LIFO |

| Items Sold | Oldest first | Newest first |

| Profit in Inflation | Higher | Lower |

| Cost of Goods Sold | Lower | Higher |

| Balance Sheet Value | Closer to market value | Often outdated |

| Tax Impact | Higher taxes | Lower taxes |

| Global Use | IFRS-approved | U.S. only |

| Real-life Analogy | Grocery shelf rotation | Warehouse pile grab |

FIFO keeps your books cleaner. LIFO can cut taxes but may distort balance sheets.

How it Hits the Books — Real-World Ripples

Numbers don’t just sit in ledgers. They move, shift, and tell stories about market changes. The method you choose decides how your costs appear when prices swing up or down. Let’s see how that plays out in real business terms.

When Prices Go Up

During inflation, costs rise with each new purchase.

- Under FIFO, old, cheaper goods sell first. Profits look bigger.

- Under LIFO, new, costlier goods sell first. Profits look smaller.

For example, if a retailer bought items at $10, then $12, and sells for $15:

- FIFO profit = $15 – $10 = $5

- LIFO profit = $15 – $12 = $3

That $2 gap can shift your tax bill.

When Prices Drop

In deflation, the effect flips. LIFO might show more profit because newer stock costs less.

Pro Tip:

The goal isn’t picking the “best” method. It’s about choosing one that fits your pricing trends and financial goals.

LIFO and FIFO Examples that Make it Click

It’s easier to understand these methods when you see them in action. Real stories from everyday businesses show how each method shapes results and decisions. Let’s walk through a few quick cases that make the difference clear.

Example 1 — The Coffee Roaster

A coffee company buys beans monthly as prices climb.

- Using FIFO, early batches cost less, so profits rise.

- Using LIFO, recent batches cost more, cutting profit but saving on taxes.

Example 2 — The Tech Retailer

A gadget store deals with fast-changing prices.

- FIFO shows consistent inventory values for investors.

- LIFO helps manage taxes when product costs spike.

Example 3 — The Ice Cream Factory

Costs melt and refreeze throughout the year.

- FIFO keeps cost records closer to actual market prices.

- LIFO helps when raw material costs increase seasonally.

These LIFO and FIFO examples show how method choice shapes a company’s story.

The Accounting Laws that Rule the Game

Inventory methods aren’t just a matter of choice. They’re also shaped by accounting rules that differ across countries. Understanding who allows what can save you from compliance headaches later on.

Who Allows What

- IFRS (International Financial Reporting Standards): Allows only FIFO.

- GAAP (U.S. Generally Accepted Accounting Principles): Allows both FIFO and LIFO.

Why it Matters

A U.S. company using LIFO may have to switch to FIFO when reporting overseas. The change can affect reported profits and tax filings.

LIFO and FIFO Examples in Action — Numbers Don’t Lie

Let’s see a small demo.

Purchases:

- 100 units @ $10

- 100 units @ $12

- 100 units @ $14

Sales: 200 units

FIFO Calculation:

COGS = $10×100 + $12×100 = $2,200

Ending inventory = $14×100 = $1,400

LIFO Calculation:

COGS = $14×100 + $12×100 = $2,600

Ending inventory = $10×100 = $1,000

Under LIFO, profits drop by $400, but so does taxable income.

These LIFO and FIFO examples prove how one choice changes your financial picture.

Which One Should You Choose?

Choosing between FIFO and LIFO isn’t about picking sides. It’s about knowing what fits your business goals, market conditions, and reporting needs. The right method depends on what story you want your numbers to tell.

It Depends on Your Goals

| Business Goal | Best Method |

| Show higher profit | FIFO |

| Reduce taxes in inflation | LIFO |

| Stay compliant worldwide | FIFO |

| Reflect the latest costs | LIFO |

Quick tips:

- FIFO is simple and easy to track.

- LIFO can reduce your tax bill, but it adds complexity.

- Your accountant can guide which method fits your growth plan.

Impact on Financial Statements

Inventory valuation affects both the income statement and the balance sheet. Understanding this impact helps decision-makers interpret financial data correctly.

Income Statement

Under FIFO, older, cheaper inventory costs are matched with current sales, leading to a lower COGS and higher net income. LIFO, using newer, higher costs, results in higher COGS and lower profits.

Balance Sheet

FIFO leaves the most recent inventory costs on the balance sheet, which better represents current market value. LIFO keeps older costs in inventory, often resulting in undervalued stock during inflation.

Both methods influence how healthy a company appears financially, even though the actual cash flow might remain the same.

The Final Note

The LIFO vs. FIFO choice isn’t about right or wrong. It’s about what fits your business best.

FIFO works well for steady prices and global reporting. LIFO suits U.S. firms facing rising costs and aiming to manage taxes.

Your method should match your market and goals. Review it often to keep your books aligned with reality.

Inventory isn’t just numbers — it’s a reflection of how your business runs. And if you’d like help keeping those numbers clear and accurate, Swyft POS offers smart accounting tools that make it simple to stay on track.

Frequently Asked Questions

1. What is the main difference between FIFO and LIFO?

FIFO assumes the oldest inventory is sold first, while LIFO assumes the newest stock is sold first. This difference affects the cost of goods sold, profit margins, and tax calculations.

2. Which method gives higher profits during inflation?

During inflation, FIFO shows higher profits because it uses older, cheaper costs for COGS. LIFO, using recent higher costs, results in lower profits but can reduce taxable income.

3. Is LIFO allowed under international accounting standards?

No. LIFO is not permitted under IFRS but is allowed under U.S. GAAP. Companies operating globally often use FIFO to maintain consistency across financial reports.

4. Can a business switch from FIFO to LIFO or vice versa?

Yes, but such changes require approval from tax authorities and proper disclosure in financial statements. Frequent switching is discouraged as it affects comparability over time.

5. Which industries typically prefer FIFO or LIFO?

FIFO is common in industries dealing with perishable or time-sensitive goods like food and pharmaceuticals. LIFO suits businesses with stable, non-perishable inventories such as oil, metals, or machinery.