If you’ve been shopping for health insurance or reviewing your benefits package, you’ve probably come across a term that sounds like it belongs in two different worlds: HMO-POS. It combines two plan types that most people already find confusing on their own, which makes the combination even harder to decode.

This guide breaks down the HMO-POS meaning in plain language, explains how it works, and covers which industries and settings rely on it most. And since POS also stands for point of sale in the business world, we’ll clarify that overlap as well. Understanding what a modern point of sale (POS) system is can also help clarify why the same acronym appears in completely different industries.

Understanding the HMO meaning early can make comparing insurance plans significantly less confusing for both patients and employers.

What Does HMO-POS Mean?

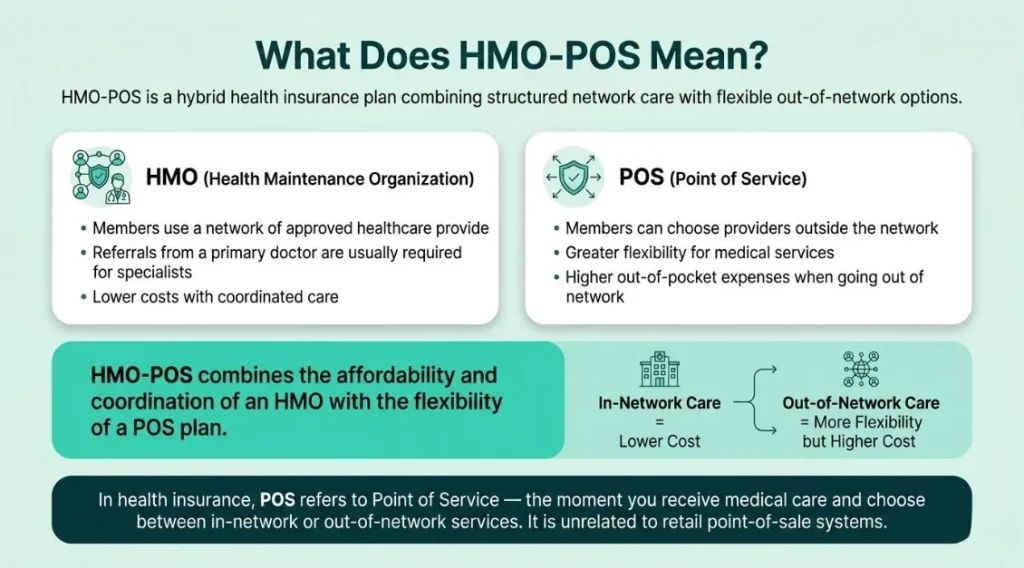

HMO-POS stands for Health Maintenance Organization with a Point of Service option. It is a type of health insurance plan that blends features of two common plan structures.

| Plan Type | What It Means |

| HMO (Health Maintenance Organization) | A plan that requires members to use a network of approved providers and get referrals from a primary care physician for specialist care |

| POS (Point of Service) | A plan that gives members the option to go outside the network for care, usually at a higher out-of-pocket cost |

An HMO-POS combines both. You get the cost efficiency and coordination of an HMO as your base, with the added flexibility to see out-of-network providers when needed. That flexibility is what the Point of Service component adds.

In the health insurance context, POS has nothing to do with retail point of sale systems. The two uses of the acronym are completely separate. POS in insurance refers to the point at which you receive medical service and the choices available to you at that moment.

How Does an HMO-POS Plan Work?

The day-to-day experience of an HMO-POS plan looks like this:

You have a Primary Care Physician

Like a standard HMO, an HMO-POS plan requires you to choose a primary care physician who coordinates your care. This doctor is your first point of contact for most health concerns and refers you to specialists when needed.

A better understanding of HMO meaning helps patients recognize why primary care coordination remains such an important part of these plans.

In-network Care is the Default

When you use in-network providers, your costs are lower, and your claims are handled like a standard HMO. This is the most cost-effective way to use the plan.

Out-of-Network Care is Available

Unlike a pure HMO, an HMO-POS allows you to see providers outside the network. The trade-off is higher out-of-pocket costs. You may need to handle more of the paperwork yourself and pay a larger share of the bill.

Referrals are Still Required for Specialists

Even when using the POS option to go out of network, most HMO-POS plans still require a referral from your primary care physician. This is one of the key differences between an HMO-POS and a PPO, where referrals are generally not required.

HMO-POS v. Other Common Plan Types

| Plan Type | Network Restriction | Referral Required | Out-of-Network Coverage | Cost Level |

| HMO | In-network only | Yes | No (emergency only) | Lowest |

| HMO-POS | In-network preferred | Yes | Yes, at higher cost | Low to medium |

| PPO | In or out of network | No | Yes, at higher cost | Medium to high |

| EPO | In-network only | No | No (emergency only) | Medium |

| HDHP | Varies | Varies | Varies | Low premium, high deductible |

Who Benefits Most from an HMO-POS Plan?

An HMO-POS plan suits people who want the lower costs of an HMO but don’t want to be completely locked into a single network. It works well for:

• People who travel frequently and may need care outside their home network area

• Patients who have existing relationships with specific out-of-network specialists they want to keep seeing

• Families who want cost-efficient everyday care but need occasional flexibility

• Anyone living in an area where the in-network provider selection is limited

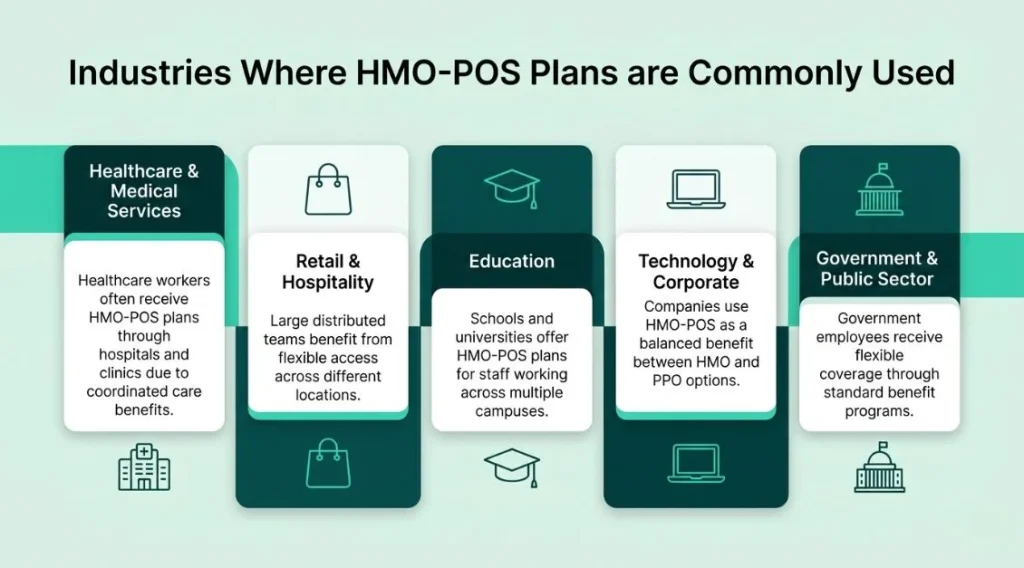

Industries Where HMO-POS Plans are Commonly Used

HMO-POS plans appear across many sectors as part of employer-sponsored benefits packages. Some industries offer them more frequently than others based on workforce needs and benefit structures.

Healthcare and Medical Services

Healthcare workers themselves are often covered by HMO-POS plans through hospital or clinic benefit packages. The plan’s emphasis on coordinated care aligns well with how healthcare professionals understand the system.

Retail and Hospitality

Large retail chains and hospitality groups with geographically spread workforces often use HMO-POS plans because the Point of Service flexibility allows employees in different locations to access care without being restricted to a single regional network.

Education

School districts and universities frequently offer HMO-POS options as part of staff benefits. The flexibility suits faculty and staff who may work across multiple campuses or travel for institutional purposes.

Technology and Corporate

Tech companies and large corporations use HMO-POS plans as a middle-ground benefit that offers more flexibility than a standard HMO without the higher premiums of a PPO, making it an attractive option for competitive benefits packages.

Government and Public Sector

Many government employee benefits programs include HMO-POS options as part of their standard benefits menu, particularly at the state and municipal level, where diverse employee populations require flexible coverage options.

HMO-POS and Point of Sale Systems: Clearing Up the Confusion

If you searched for HMO-POS and landed somewhere that talks about retail point of sale systems, the confusion is understandable. POS is one of those acronyms that does double duty in different industries.

| Context | What POS Stands For | What It Refers To |

| Health insurance | Point of Service | The option to receive care inside or outside your insurance network |

| Retail and business | Point of Sale | The system used to process customer payments and manage transactions |

In the business world, a POS system like Swyft POS is the technology that powers transactions at the checkout counter, whether that’s in a restaurant, retail store, salon, or any other customer-facing business. If you’re unfamiliar with how these systems work, this guide on what a POS system is and why it’s essential for businesses explains the fundamentals clearly.

For readers trying to understand how payment processing works behind these systems, this guide on POS transaction meaning, types, and how it works explains the process in more detail.

Pros and Cons of an HMO-POS Plan

| Pros | Cons |

| Lower premiums than PPO plans | Referrals still required for specialists |

| Flexibility to see out-of-network providers | Out-of-network care costs significantly more |

| Coordinated care through a primary physician | More paperwork when using out-of-network options |

| Good balance of cost and flexibility | Not as flexible as a full PPO |

| Useful for people who travel or live in multiple areas | Network limitations still apply for in-network pricing |

Final Thoughts

An HMO-POS plan sits in a practical middle ground in the health insurance landscape. It keeps costs lower than a PPO while giving members more freedom than a standard HMO. For people who value coordinated care but don’t want to be completely restricted to one network, it is often one of the more sensible choices available.

Understanding the HMO meaning and how the Point of Service component adds flexibility helps you make a more informed decision when comparing health plan options during open enrollment or when evaluating a new employer’s benefits package.

If you’re looking for a smarter way to manage payments, inventory, and customer transactions, contact us to learn how the right POS system can support your business growth.

FAQs

1. What does HMO-POS mean?

HMO-POS stands for Health Maintenance Organization with a Point of Service option. It is a health insurance plan that combines the cost efficiency and coordinated care of an HMO with the flexibility to see out-of-network providers at a higher cost.

2. How is an HMO-POS different from a standard HMO?

A standard HMO restricts members to in-network providers only, with no coverage for out-of-network care except in emergencies. An HMO-POS adds a Point of Service option that allows members to use out-of-network providers when needed, though at a higher out-of-pocket cost.

3. Do I still need referrals with an HMO-POS plan?

Yes. Most HMO-POS plans still require a referral from your primary care physician to see a specialist, whether in-network or out-of-network. This is one of the key differences between an HMO-POS and a PPO plan.

4. Is POS in HMO-POS the same as a retail POS system?

No. In the health insurance context, POS stands for Point of Service, referring to the flexibility to choose between in-network and out-of-network care. In retail and business, POS stands for Point of Sale and refers to payment processing systems. The two uses of the acronym are completely unrelated.

5. Which industries commonly offer HMO-POS plans?

HMO-POS plans are commonly offered in healthcare, retail, hospitality, education, technology, and government sectors. They are particularly popular among employers with geographically distributed workforces who need flexible coverage options for employees in different locations.